𝐀 𝐛𝐫𝐞𝐚𝐜𝐡 𝐨𝐟 𝐭𝐫𝐮𝐬𝐭 𝐛𝐲 𝐭𝐡𝐞 𝐅𝐚𝐢𝐫𝐛𝐚𝐧𝐤𝐬 𝐒𝐜𝐡𝐨𝐨𝐥 𝐃𝐢𝐬𝐭𝐫𝐢𝐜𝐭

Surplus funds subject to limit imposed by borough of 40% of their contribution to the school district

As you may recall, earlier this year as the result of an external audit there was a “clawback” by the borough from the school district of $11.4M of excess surplus at the end of the 24-25 fiscal year (borough ordinance 7.04.125, finalized in 2018), and this was made public in late January. FNSBSD has claimed multiple times it could not have foreseen this excess surplus because they could not have known that multiple categories of expenditures would be underspent until it was too late to do anything about it. Despite repeated requests by parents and the borough assembly, the district and school board have refused to provide a report with the month-by-month account details that would be required to substantiate those claims.

Why does the borough, and why should you, not want the school district building up a giant savings account? More than many things in life, a child’s education is a “here and now” activity. Children will never get back the years where their elementary school did not have instrumental music, or the years where they did not learn as much because their teacher struggled to maintain control of an oversized class.

The only real insight we can gain into this issue is to wade through the year-end financial reports of the school district to see year-over-year changes in the borough surplus. Those reports are called the Annual Comprehensive Financial Reports (ACFR). After an initial Facebook post discussing the budget surplus of the school district, someone very familiar with the school district budget contacted me to correct me regarding exactly which funds are used for the calculation that is compared to 40% of the borough’s contribution. I thank this person, as I would never have gotten it exactly right from the financial report myself. With the page numbers in the 24-25 ACFR in parentheses, the calculation is as follows:

Total assigned funds (p 37, 1st col)

- Impact aid advance (p 37, 1st col)

+ Unassigned funds (p 37, 1st col)

+ Total assigned Student Transportion Special Revenue Fund (p 37, 2nd col)

+ Total committed Nonmajor Governmental Funds (p 37, 4th col)

+ Net position - ending, Risk Management Internal Service Fund (p 127, 1st col)

+ Net position - ending, Equipment Replacement Internal Service Fund (p 131, 1st col).

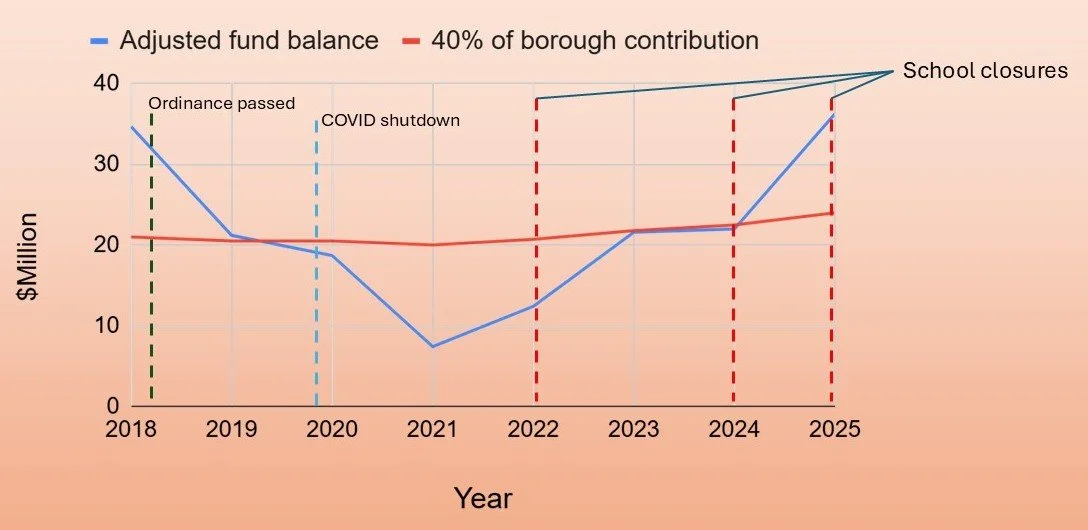

In the graph I show the correct calculation as “Adjusted Fund Balance”. If this value exceeds 40% of the borough’s contribution to the school district for the fiscal year, then the borough ordinance requires that the excess funds be returned. The person that contacted me thought it was very important to note that the borough itself maintains much larger year-end fund balances than the school district, and he thought this was hypocritical of the borough.

What you can clearly see is that the 2024-2025 excess surplus was not some sudden spike in the district’s funds. Instead, following a COVID-caused depletion there was a consistent buildup of funds of several million dollars per year that raised savings to almost exactly what is allowed by the ordinance before the final clawback by the borough. In other words, the district was squirreling away millions per year while schools were being closed and a variety of other extreme austerity measures were being implemented. The borough was also adjusting its budget so that it could increase the borough contribution to a school district claiming acute financial difficulty. It is hard to believe that this surplus accrual was accidental and not the intentional result of consistently overbudgeting in different expense categories. For example, there are five straight years where the categories of “special education instruction” and “operations and maintenance of plant” were overbudgeted (p. 63 of 24-25 ACFR), with the average amount being $1.6M and $1.7M per year, respectively.

Note that even during COVID that these surplus funds did not get below $7M. The claim that opening a charter school would somehow jeopardize funding for other district priorities clearly does not hold water.

To me this looks like a betrayal of trust of an entire community that rallied around a school district that claimed it was all but bankrupt.